Projects

India and global projects in quantitative finance, portfolio construction, and systematic investing — sorted by newest first.

Each project applies quantitative methods to a specific problem in finance — from clustering-based portfolio construction and market regime detection to adaptive portfolio strategies and RRG-based rotation analysis.

Projects include interactive visualizations, source code links, and methodology explanations. Data is updated periodically via automated pipelines.

| 25. |  Momentum Rebalance Frequency Study

(2026 )

12-1 momentum on US large caps across semi-annual, quarterly, monthly, and weekly rebalance cadences — turnover, net Sharpe, and implementation efficiency. 12-1 momentum · semi-annual · quarterly · monthly · weekly · turnover · cost scenarios |

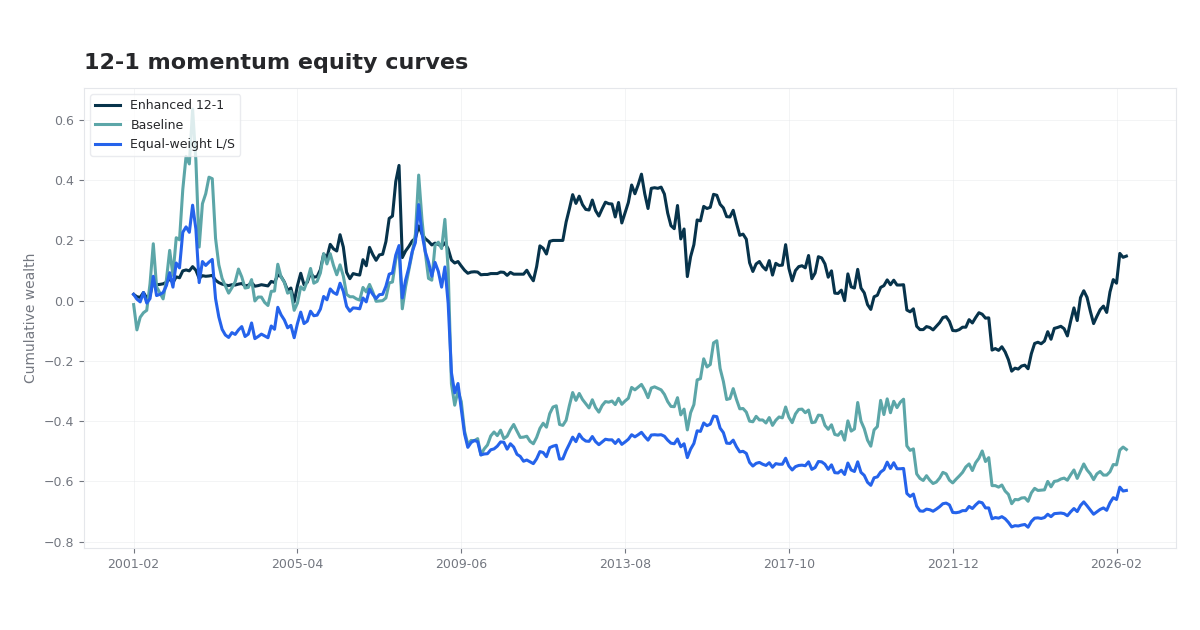

| 26. |  Cross-Sectional 12-1 Momentum in S&P 500

(2026 )

Jegadeesh-Titman 12-1 momentum on US large caps: alpha persistence, regime dependence, crash risk, vol-managed overlays, factor decomposition, and ML crash prediction. yfinance · decile sorts · CAPM/FF/Carhart · regime · ML crashes |

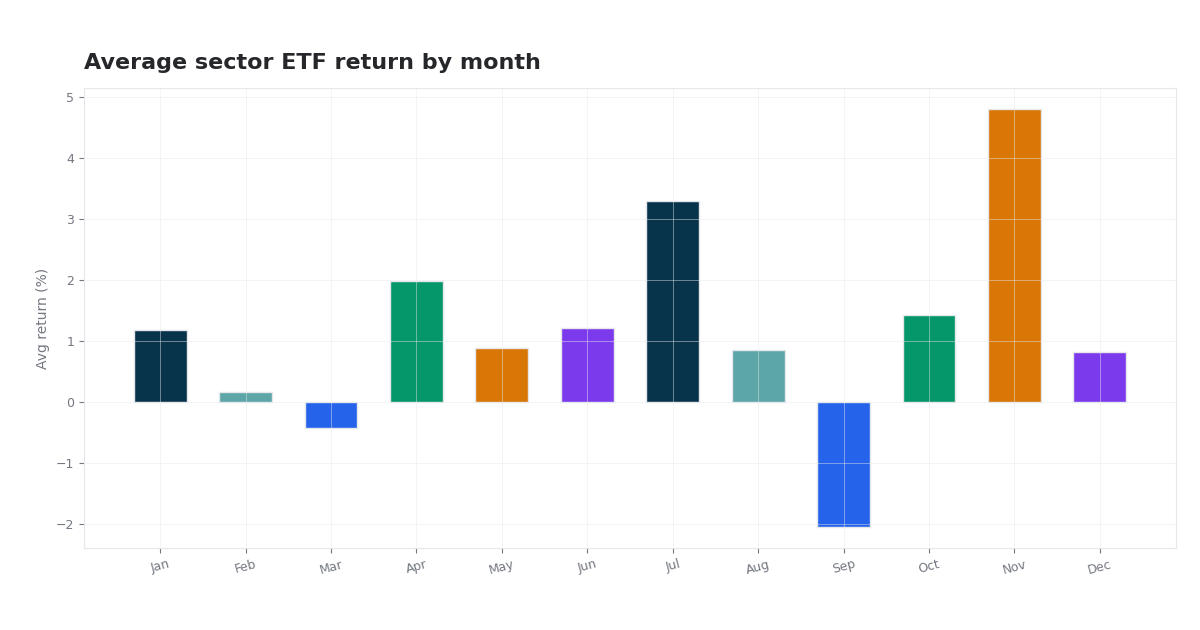

| 27. |  Calendar Effects in US GICS Sector ETFs

(2026 )

Empirical seasonality framework for eleven SPDR GICS sector ETFs vs SPY: calendar-month averages, cyclical vs defensive dispersion, benchmark-relative rotation, and exploratory inference. yfinance · SPDR sector ETFs · calendar seasonality · t-tests |

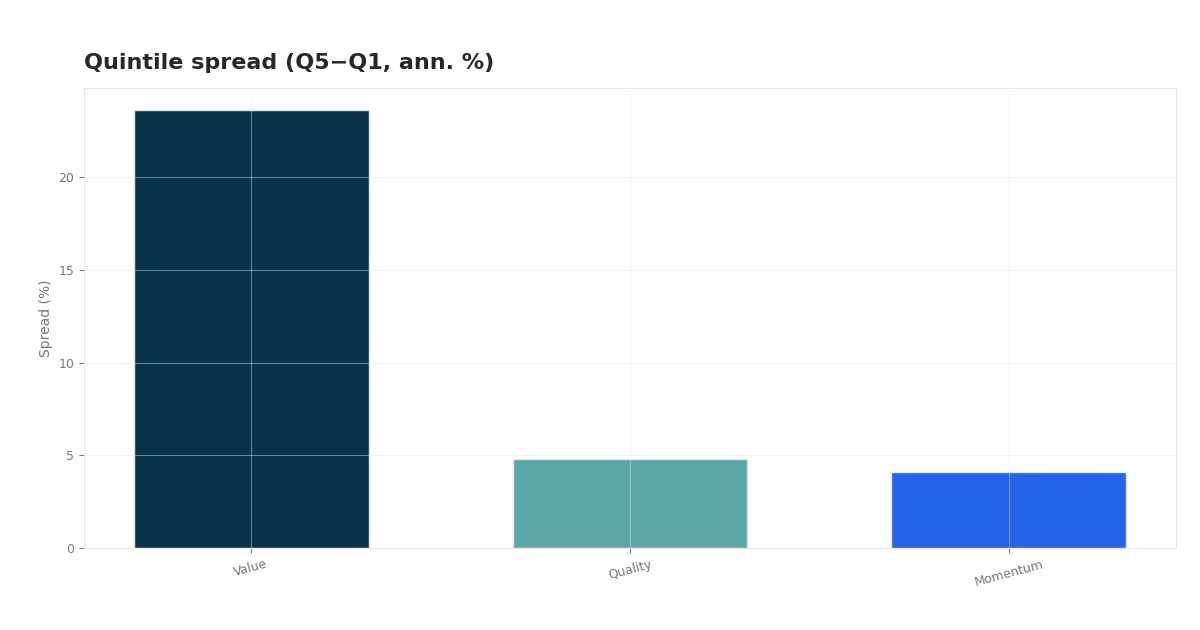

| 28. |  US Multi-Factor Risk & Return Model

(2026 )

Value, Quality, and Momentum on a US large-cap panel with nonlinear spec tests, IC/quintile diagnostics, and return attribution. Panel OLS, model selection, IC, quintiles, attribution |

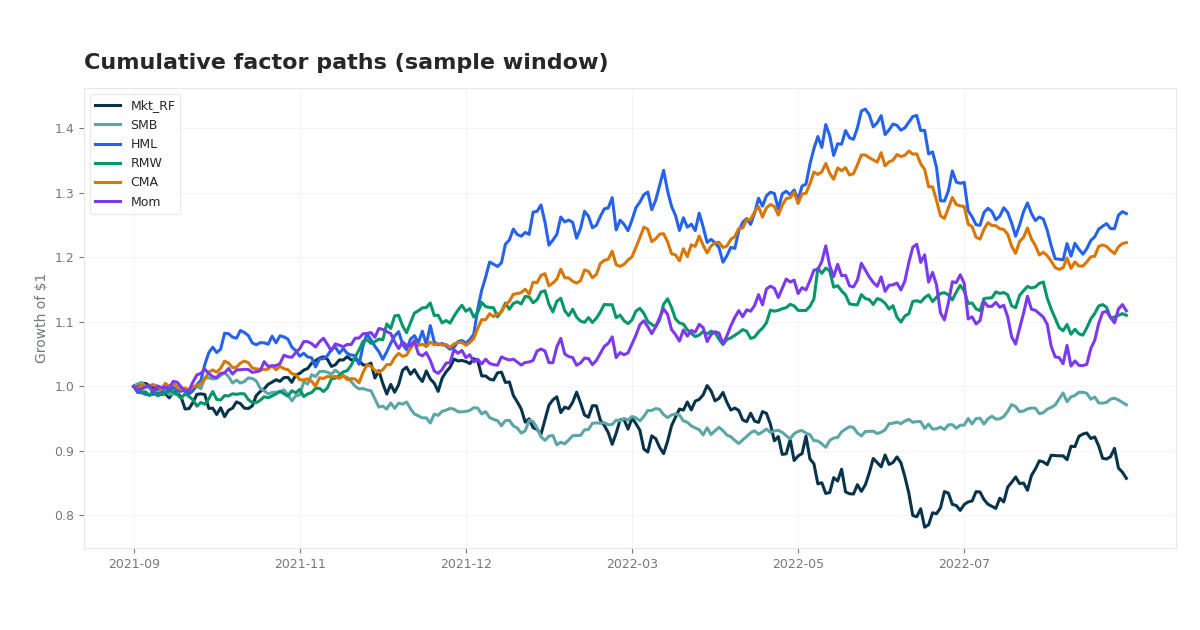

| 29. |  Fama–French Factor Lab

(2026 )

Unified factor dashboard: US FF5 and Carhart momentum, multi-asset ETF panel, international sleeve comparison, volatility regimes, risk budgeting, sleeve attribution, SPY research grid, and q-factor extension notes. Refreshed from Ken French + yfinance. Python, pandas, linear factor models, Ken French data, yfinance |

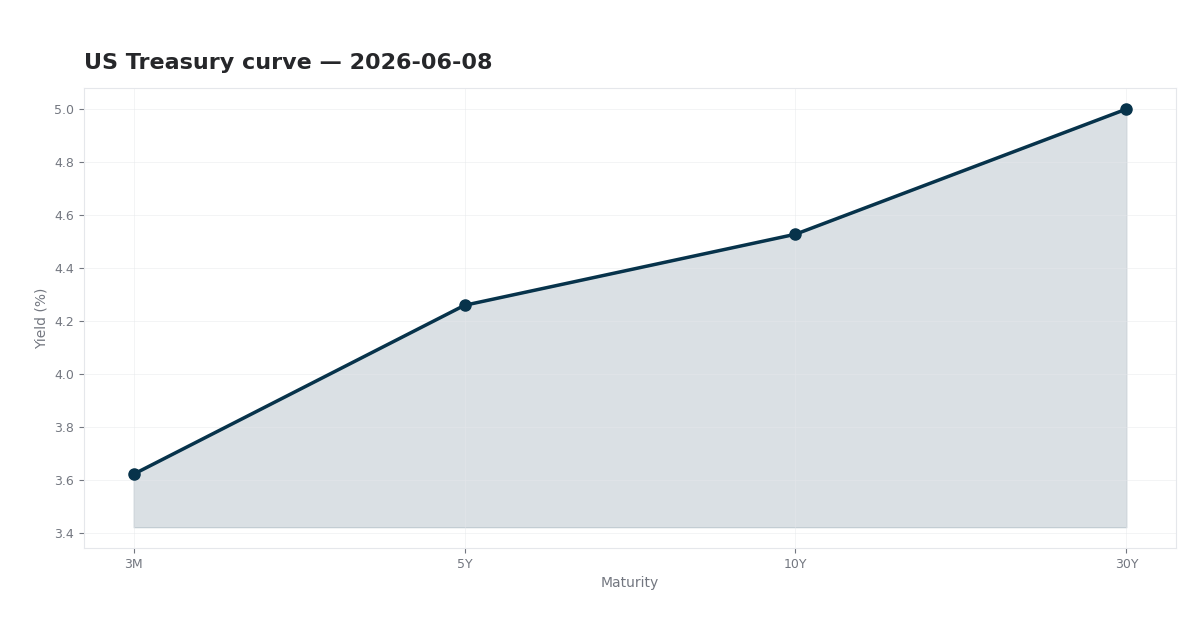

| 30. |  Yield Curve Intelligence

(2026 )

Yield-curve research project built from yfinance market data: Nelson-Siegel fitting, slope/inversion diagnostics, and regime-aware risk context. Python, yfinance, Nelson-Siegel, macro risk signals |

| 31. | Stock Sentiment Tracker

(2025 )

US equity sentiment tracker using VADER lexical analysis on financial news headlines. Tracks prices, sentiment scores, and correlations for S&P 500 stocks. Updated daily. Python, VADER, NLP, financial news APIs |

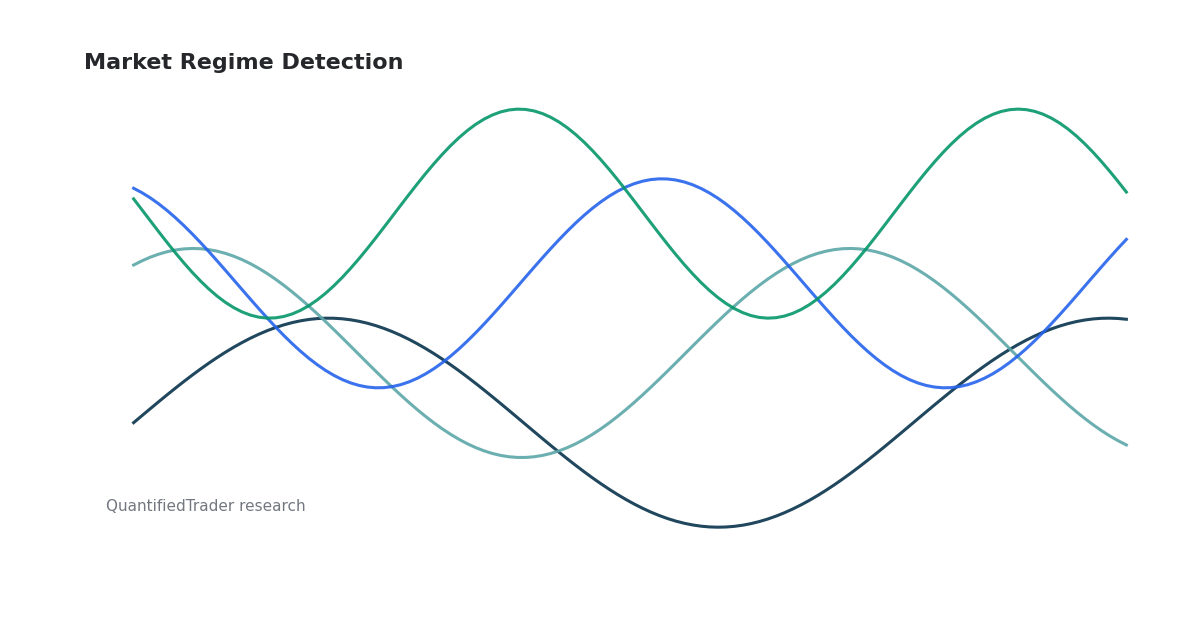

| 32. |  Market Regime Detection Using Gaussian Models

(2025 )

Comprehensive market regime identification across 21 global indices using Gaussian Mixture Models (GMM) and Greedy Gaussian Segmentation (GSS). Detects bull, bear, and transition regimes for adaptive portfolio management. Python, GMM, GSS, regime detection |

Showing 25–32 of 40 projects