Projects

India and global projects in quantitative finance, portfolio construction, and systematic investing — sorted by newest first.

Each project applies quantitative methods to a specific problem in finance — from clustering-based portfolio construction and market regime detection to adaptive portfolio strategies and RRG-based rotation analysis.

Projects include interactive visualizations, source code links, and methodology explanations. Data is updated periodically via automated pipelines.

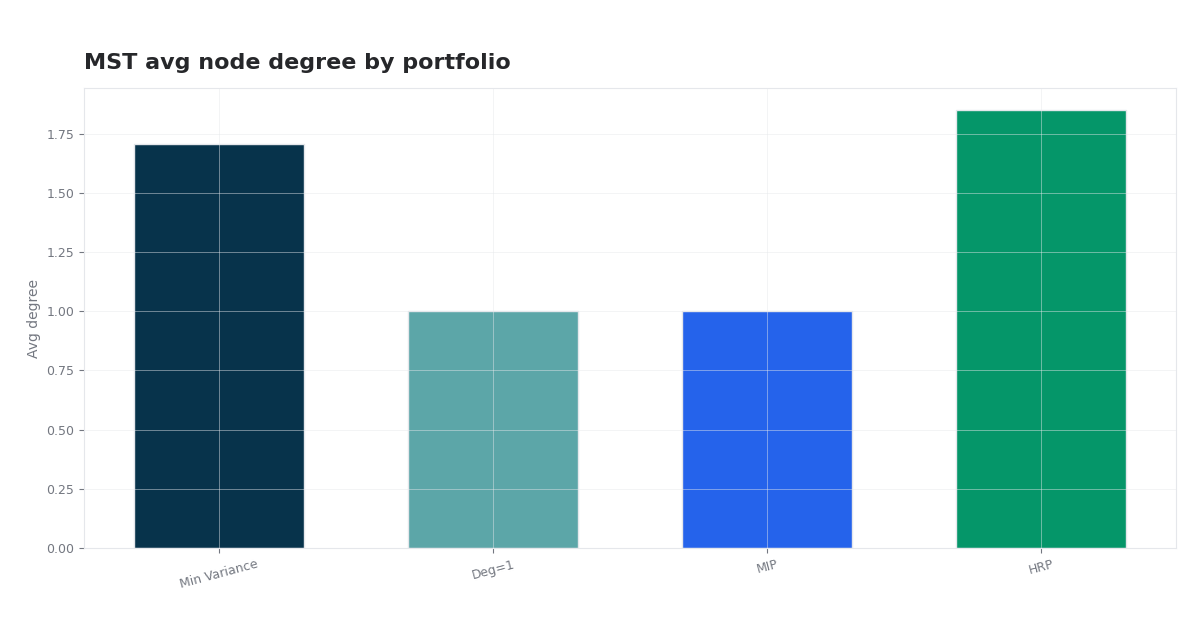

| 1. |  Nifty 50 Graph-Constrained Portfolio Optimization

(2026 · India)

MST and TMFG networks on Nifty 50 with average-centrality and neighborhood constraints inside mean–variance programs, compared with HRP, HERC, and NCO. MST · TMFG · Centrality · Neighborhood MIP |

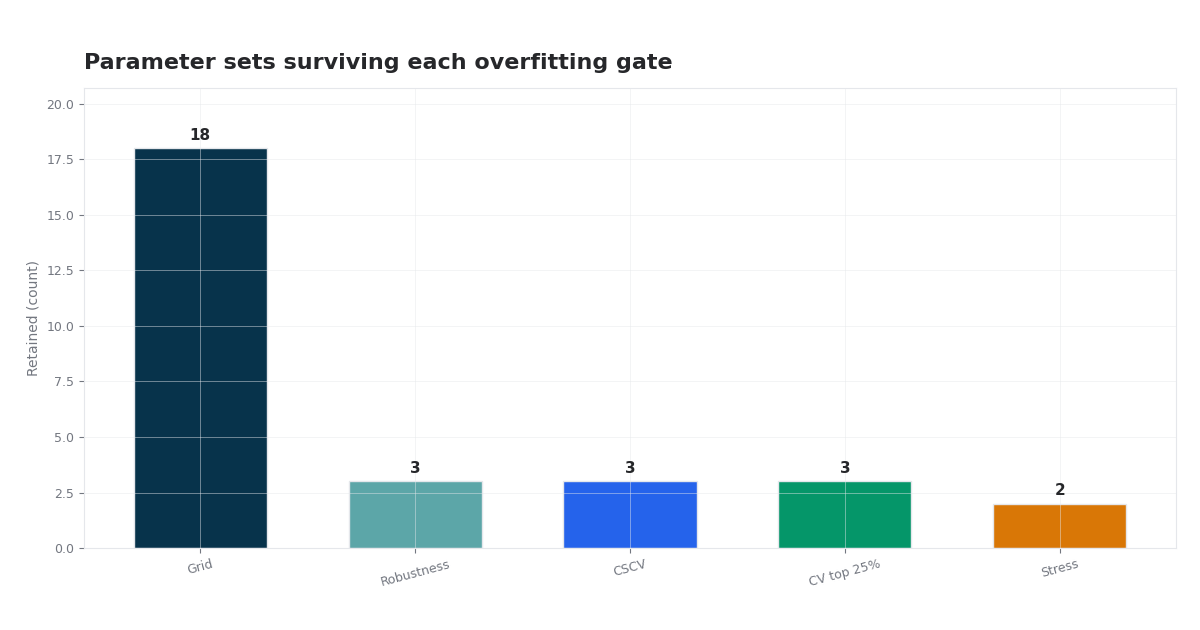

| 2. |  Detecting Overfitting in Momentum Strategies

(2026 )

Multi-stage overfitting diagnostics for S&P 500 J/K/N winners-only momentum: DSR, disparity, sensitivity, block bootstrap, CSCV/PBO, walk-forward CV, and stress-tested selection. J/K/N · Deflated Sharpe · CSCV/PBO · walk-forward · stress tests |

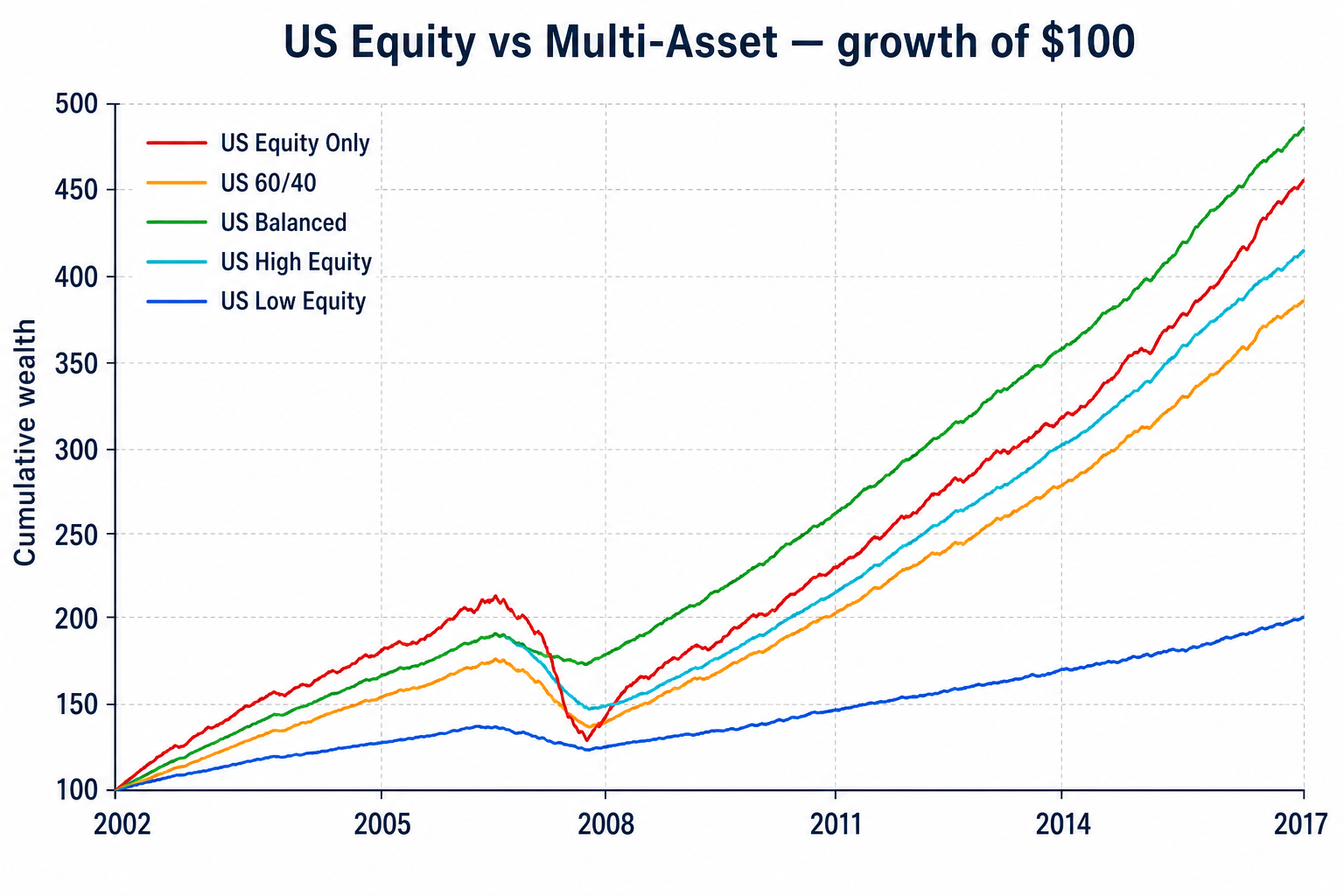

| 3. |  US Equity vs US Multi-Asset Risk-Adjusted Study

(2026 )

Comparative allocation study of US equity-only versus US multi-asset portfolios (stocks, bonds, REITs) with hypothesis testing, frontier diagnostics, and interactive risk-adjusted analytics. US equity · US bonds · REITs · Sharpe tests · drawdown tests · interactive diagnostics |

| 4. |  India Six-Factor Premia, Attribution & Regime Analysis

(2026 · India)

Six-factor study of Indian equities: long-run premia, Nifty style-index regressions, momentum crash risk, mutual-fund attribution, and whether quality pays in downturns — with interactive charts. FF6 · Nifty indices · Fund attribution |

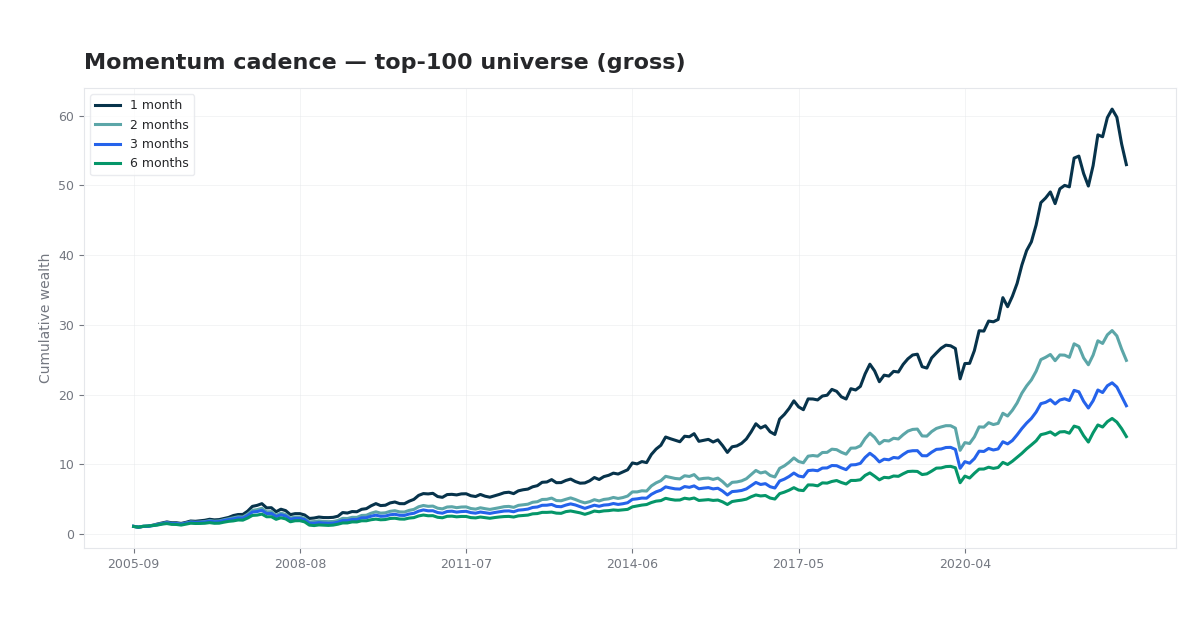

| 5. |  Momentum Cadence and Portfolio Design in Indian Equities

(2026 · India)

A systematic grid study of long-only 12-1 momentum on Indian equities: how rebalance interval, universe breadth, holdings count, and weighting scheme interact — with overlapping portfolios, transaction costs, and six-factor attribution. 12-1 momentum · 144 configurations · net of costs |

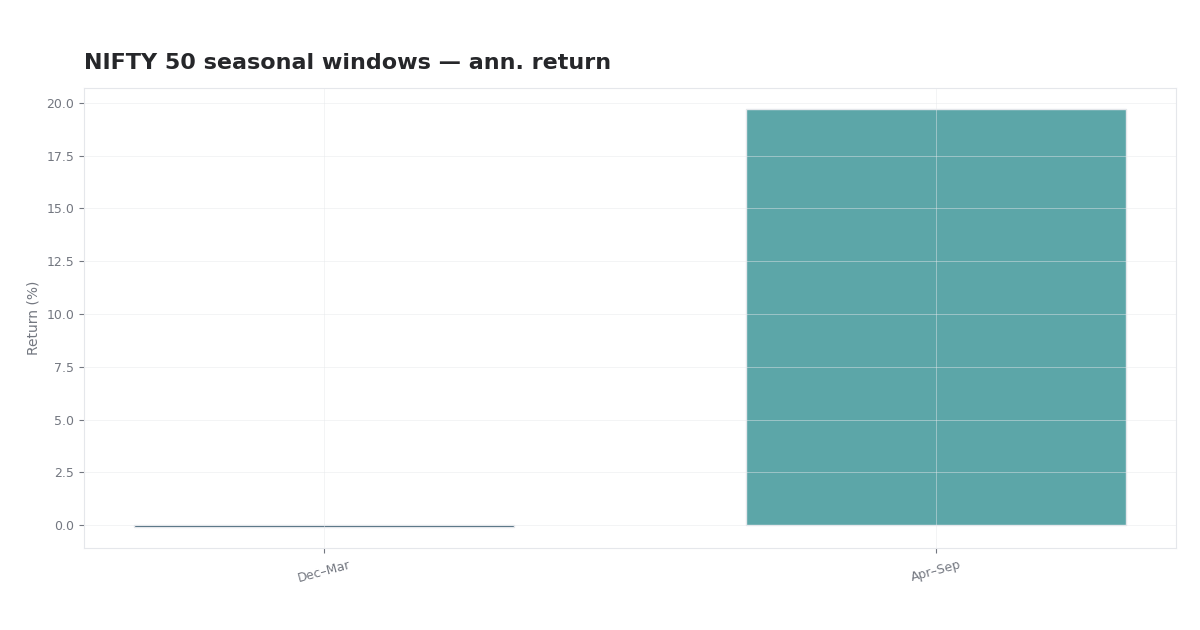

| 6. |  NIFTY 50 Seasonal Analysis by Industry & SARIMA

(2026 · India)

Report on NIFTY 50 calendar seasonality by industry: equal-weight sector baskets, cyclical vs defensive cycle spreads, benchmark-relative correlation, and SARIMA index diagnostics with full mathematical framework. Sector baskets · Industry cycle · SARIMA |

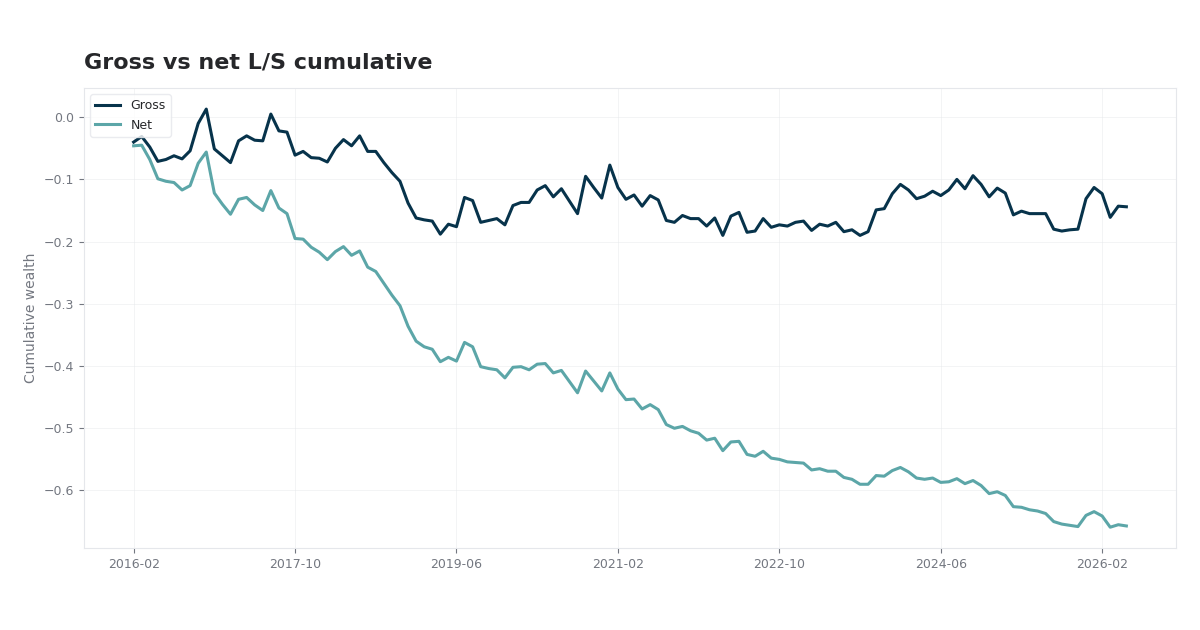

| 7. |  Nifty 50 Value-Momentum-Size Long-Short Strategy

(2026 · India)

Nifty 50 Value, Momentum, and Size: Fama–MacBeth premia, IC/IR, and a 20%/20% long–short backtest on NSE data via yfinance — with interactive performance charts. Nifty 50 · Fama–MacBeth · L/S |

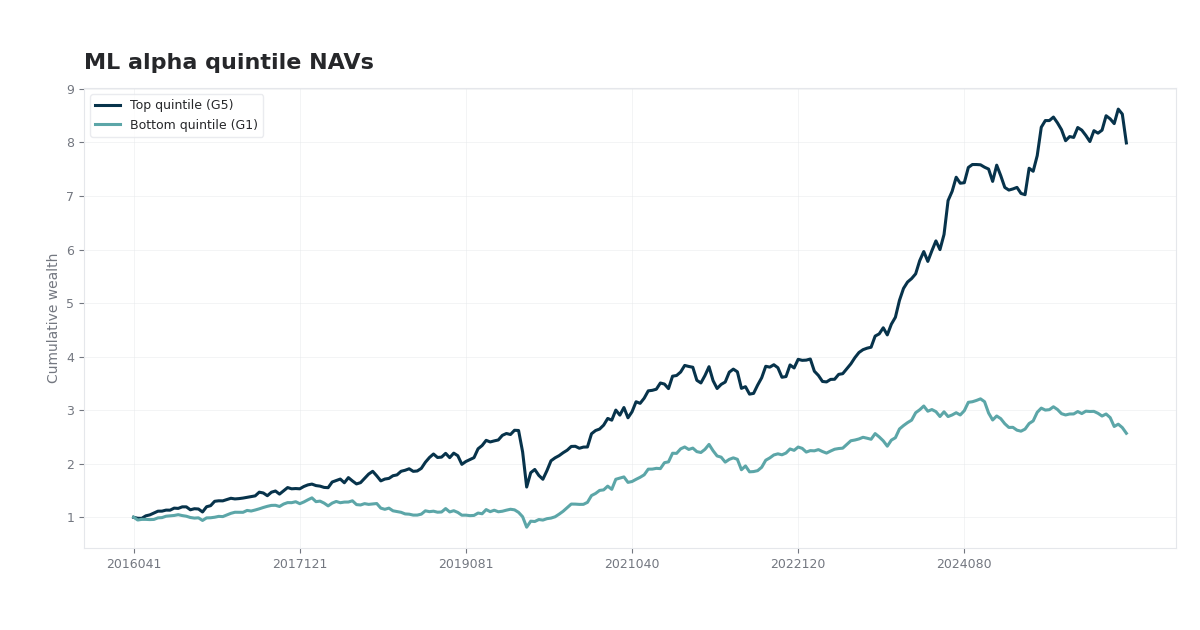

| 8. |  Nifty 50 Alpha101 Selection & Composite Factor Research

(2026 · India)

Formulaic alphas on Nifty 50: cross-sectional cleaning, IC screening, linear and machine-learning composites, and quintile backtests — full research report with interactive charts. Alpha101 · IC · L/S quintiles |

Showing 1–8 of 40 projects