India Research

Research on Indian equities through the lens of modern factor investing — size, value, profitability, investment, and momentum — applied to Nifty benchmarks and fund returns. Open a project for context, methodology, and interactive results.

Projects

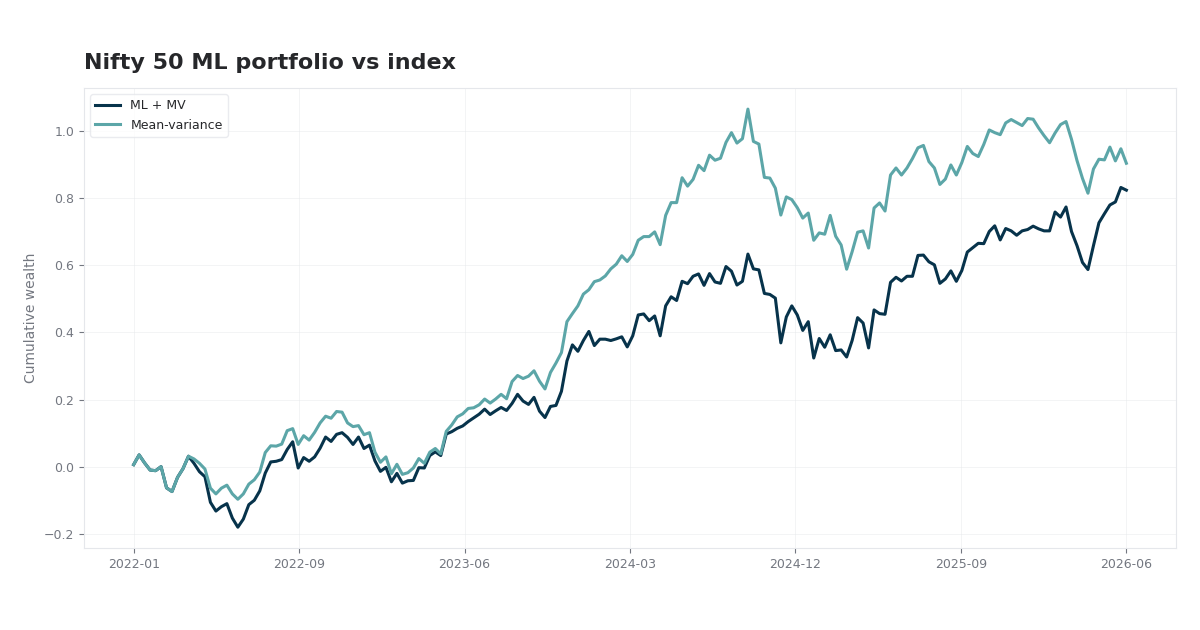

| 1. |  Nifty 50 ML-Enhanced Portfolio Optimization Mean-variance and machine-learning return views blended via Black-Litterman on Nifty 50: walk-forward backtest versus cap-weight and the index, with sector allocation and cross-sectional signals. | 2026 |

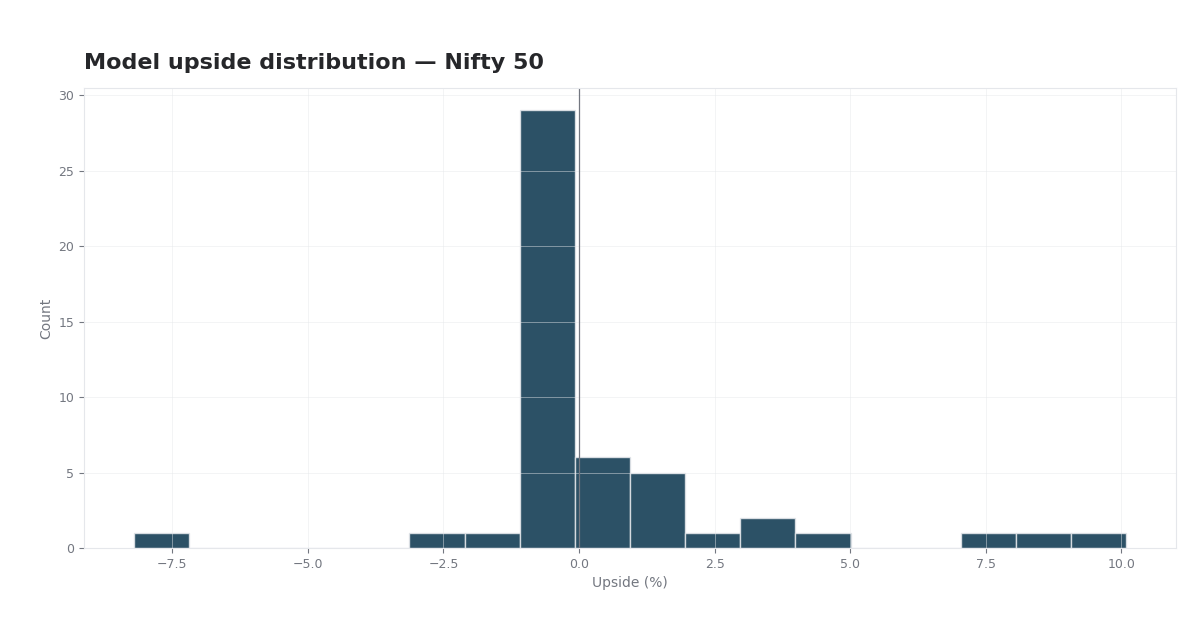

| 2. |  Nifty 50 Discounted Cash Flow Valuation Discounted cash flow valuation for every Nifty 50 name: shared India macro assumptions, WACC, terminal value, and model upside versus market price. | 2026 |

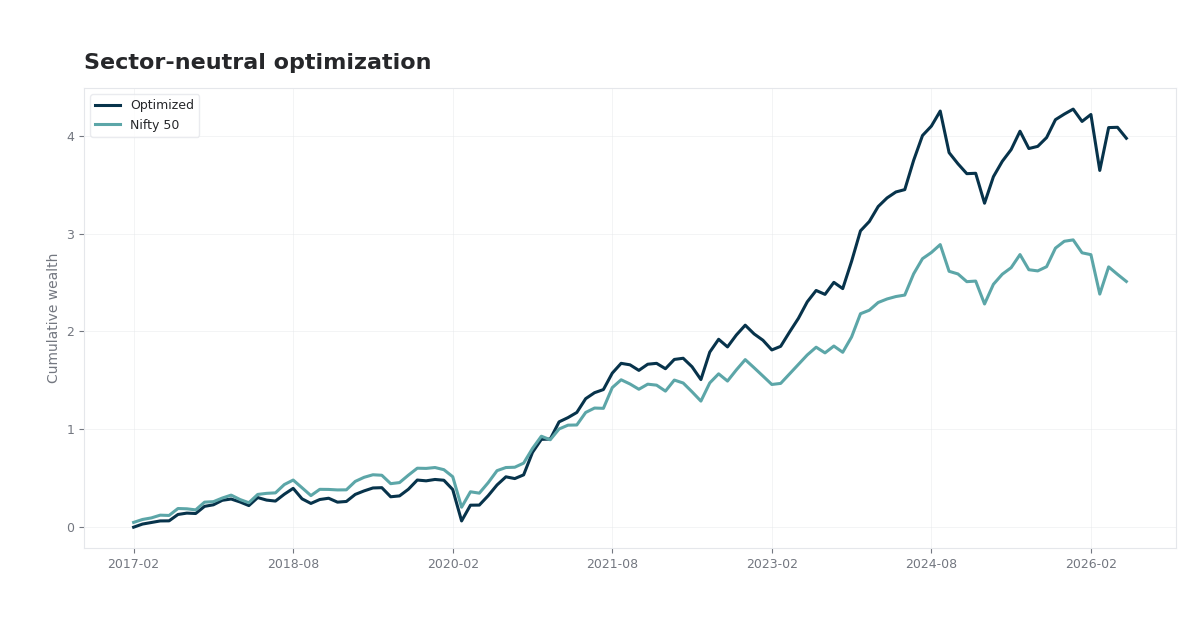

| 3. |  Nifty 50 Multi-Factor Risk Model & Sector-Neutral Optimization Research report: daily style and sector risk factors on Nifty 50, rolling WLS covariance, and monthly sector-neutral long-only optimization with turnover costs. | 2026 |

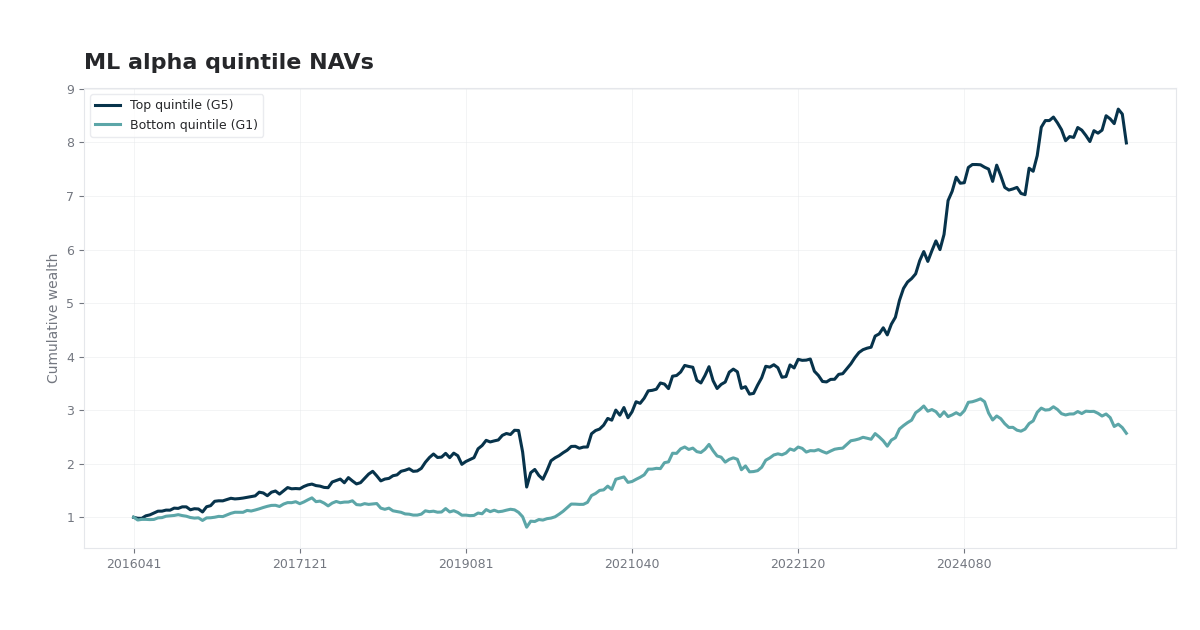

| 4. |  Nifty 50 Alpha101 Selection & Composite Factor Research Formulaic alphas on Nifty 50: cross-sectional cleaning, IC screening, linear and machine-learning composites, and quintile backtests — full research report with interactive charts. | 2026 |

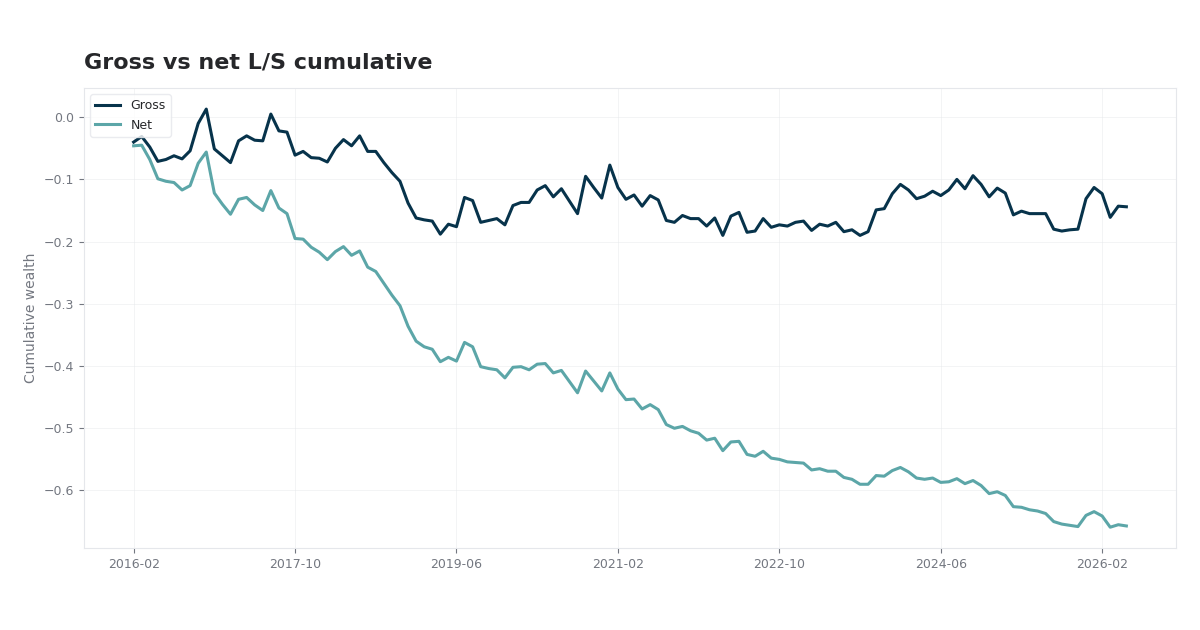

| 5. |  Nifty 50 Value-Momentum-Size Long-Short Strategy Nifty 50 Value, Momentum, and Size: Fama–MacBeth premia, IC/IR, and a 20%/20% long–short backtest on NSE data via yfinance — with interactive performance charts. | 2026 |

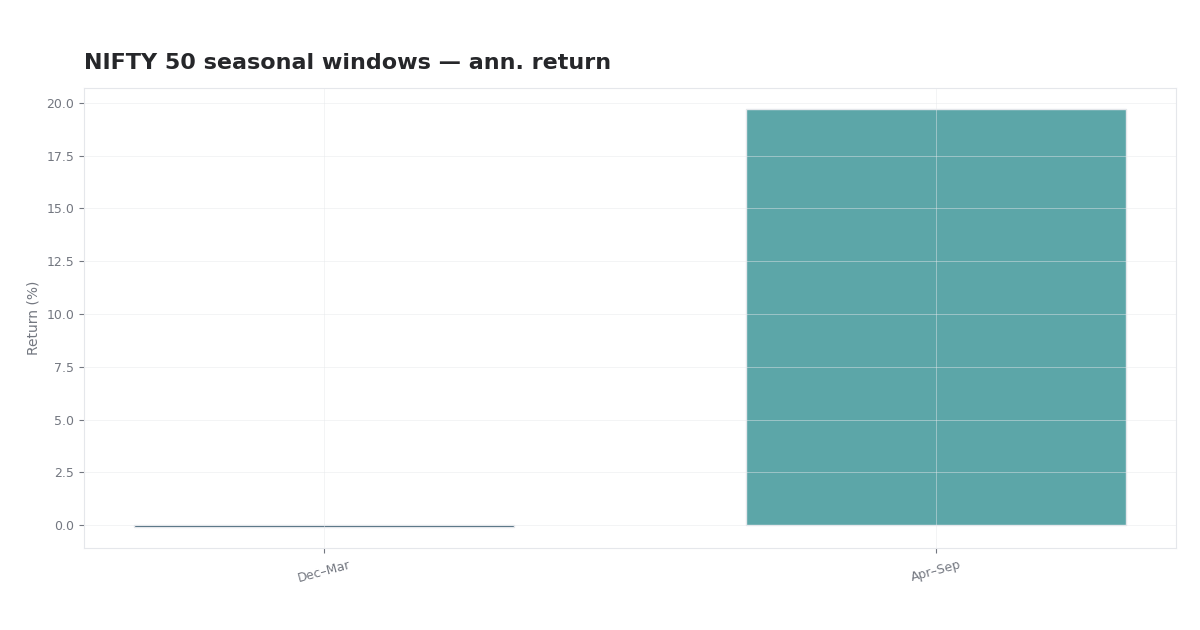

| 6. |  NIFTY 50 Seasonal Analysis by Industry & SARIMA Report on NIFTY 50 calendar seasonality by industry: equal-weight sector baskets, cyclical vs defensive cycle spreads, benchmark-relative correlation, and SARIMA index diagnostics with full mathematical framework. | 2026 |

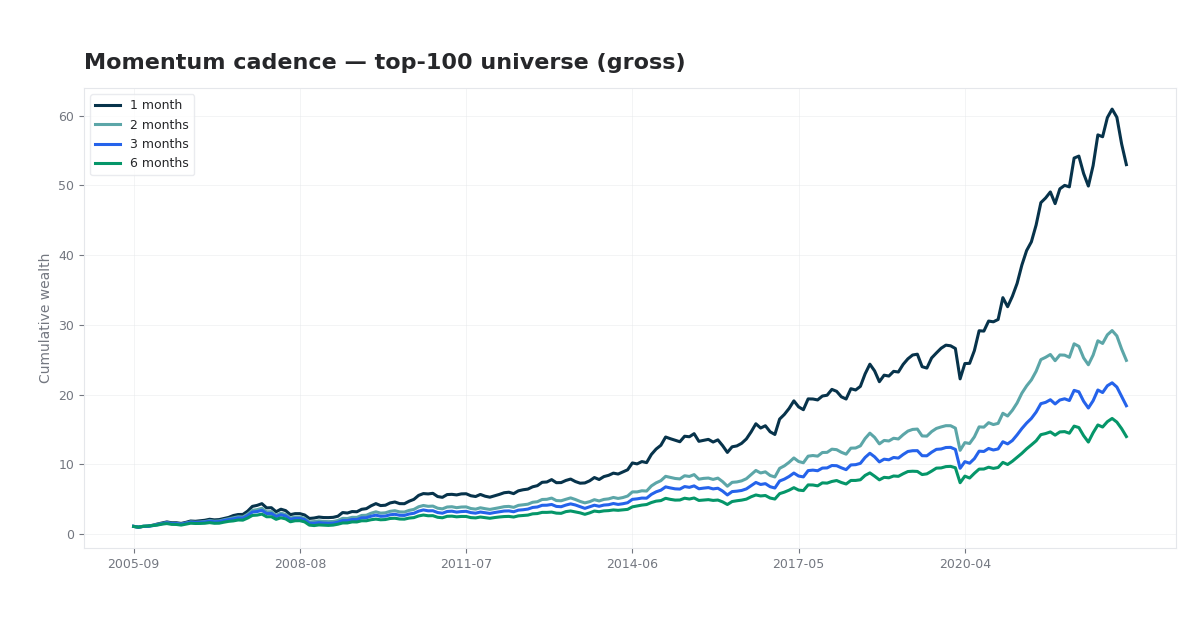

| 7. |  Momentum Cadence and Portfolio Design in Indian Equities A systematic grid study of long-only 12-1 momentum on Indian equities: how rebalance interval, universe breadth, holdings count, and weighting scheme interact — with overlapping portfolios, transaction costs, and six-factor attribution. | 2026 |

| 8. |  India Six-Factor Premia, Attribution & Regime Analysis Six-factor study of Indian equities: long-run premia, Nifty style-index regressions, momentum crash risk, mutual-fund attribution, and whether quality pays in downturns — with interactive charts. | 2026 |

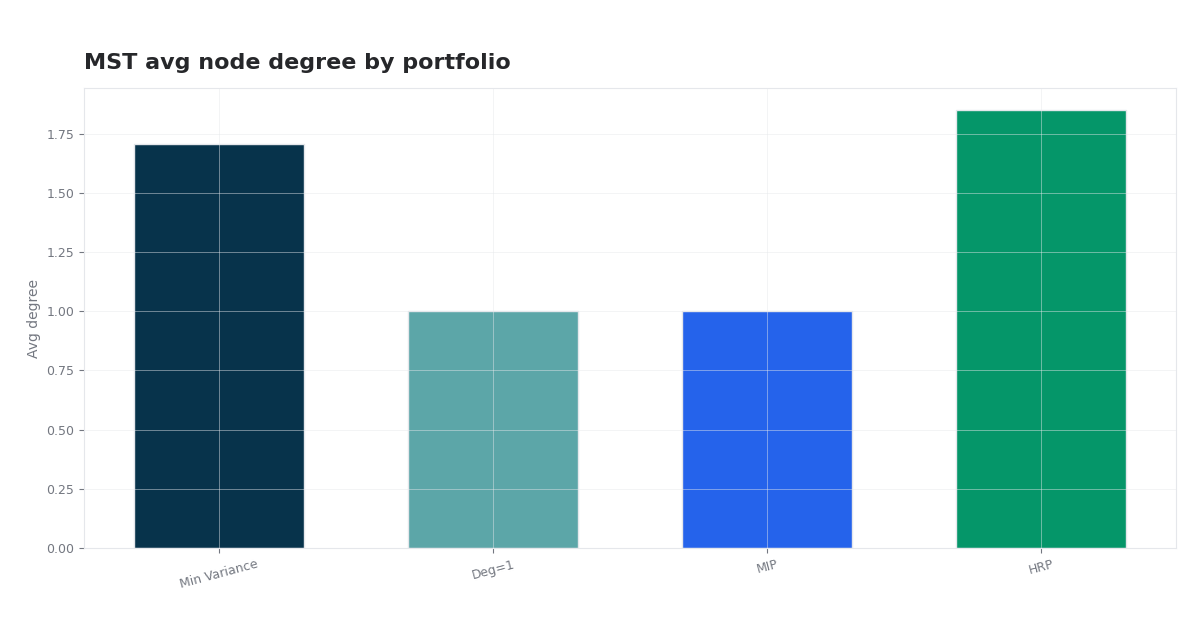

| 9. |  Nifty 50 Graph-Constrained Portfolio Optimization MST and TMFG networks on Nifty 50 with average-centrality and neighborhood constraints inside mean–variance programs, compared with HRP, HERC, and NCO. | 2026 |

Global projects (US indices, options, clustering) remain on the main projects page.