Projects

India and global projects in quantitative finance, portfolio construction, and systematic investing — sorted by newest first.

Each project applies quantitative methods to a specific problem in finance — from clustering-based portfolio construction and market regime detection to adaptive portfolio strategies and RRG-based rotation analysis.

Projects include interactive visualizations, source code links, and methodology explanations. Data is updated periodically via automated pipelines.

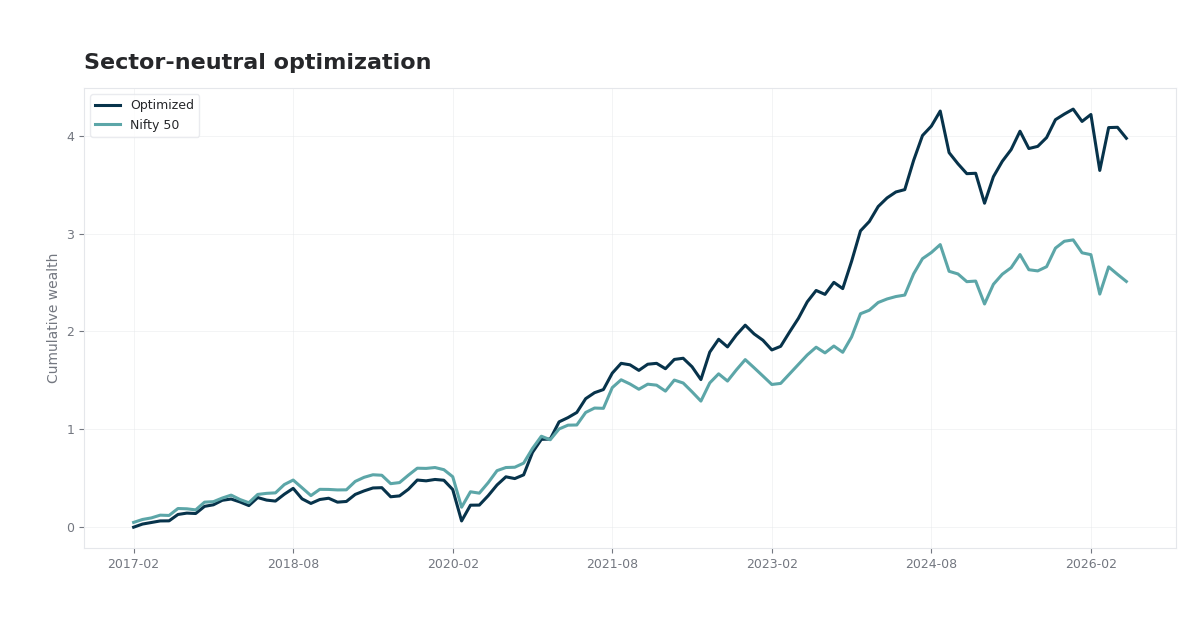

| 9. |  Nifty 50 Multi-Factor Risk Model & Sector-Neutral Optimization

(2026 · India)

Research report: daily style and sector risk factors on Nifty 50, rolling WLS covariance, and monthly sector-neutral long-only optimization with turnover costs. Risk model · Optimization · Backtest |

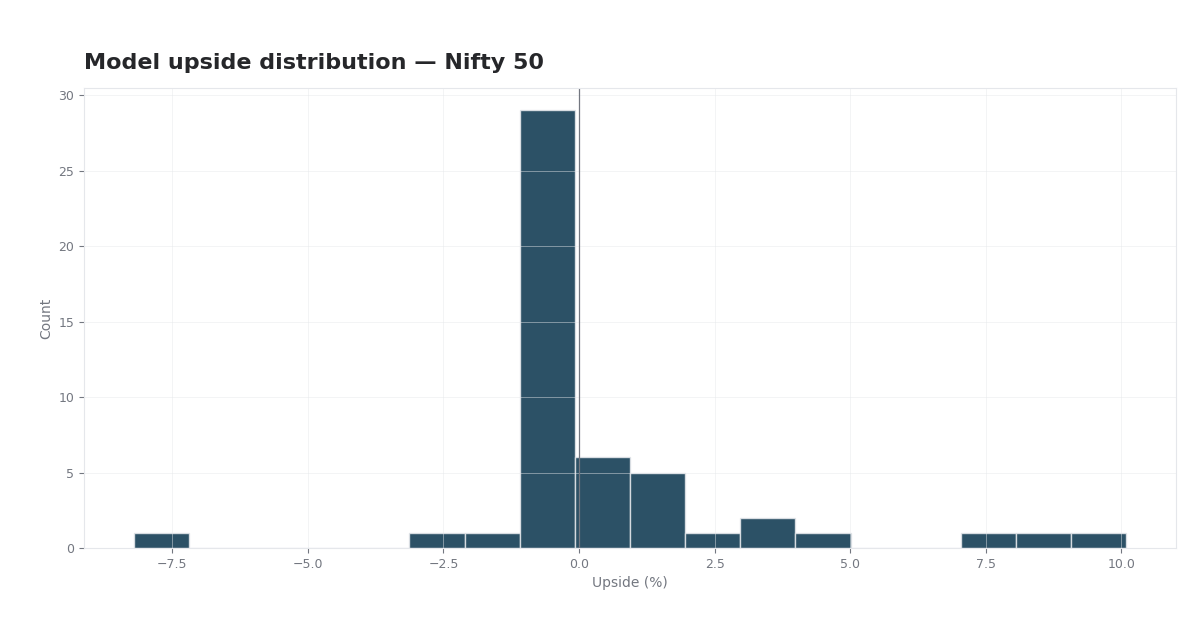

| 10. |  Nifty 50 Discounted Cash Flow Valuation

(2026 · India)

Discounted cash flow valuation for every Nifty 50 name: shared India macro assumptions, WACC, terminal value, and model upside versus market price. DCF · WACC · FCFF · Nifty 50 |

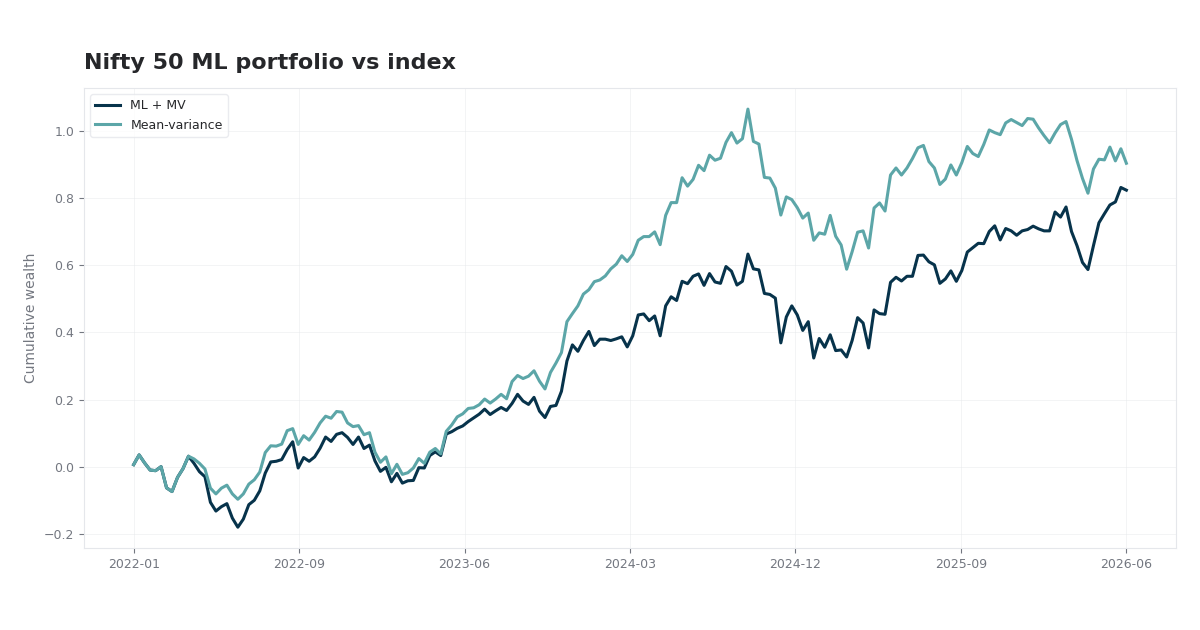

| 11. |  Nifty 50 ML-Enhanced Portfolio Optimization

(2026 · India)

Mean-variance and machine-learning return views blended via Black-Litterman on Nifty 50: walk-forward backtest versus cap-weight and the index, with sector allocation and cross-sectional signals. MVO · XGBoost · Black-Litterman |

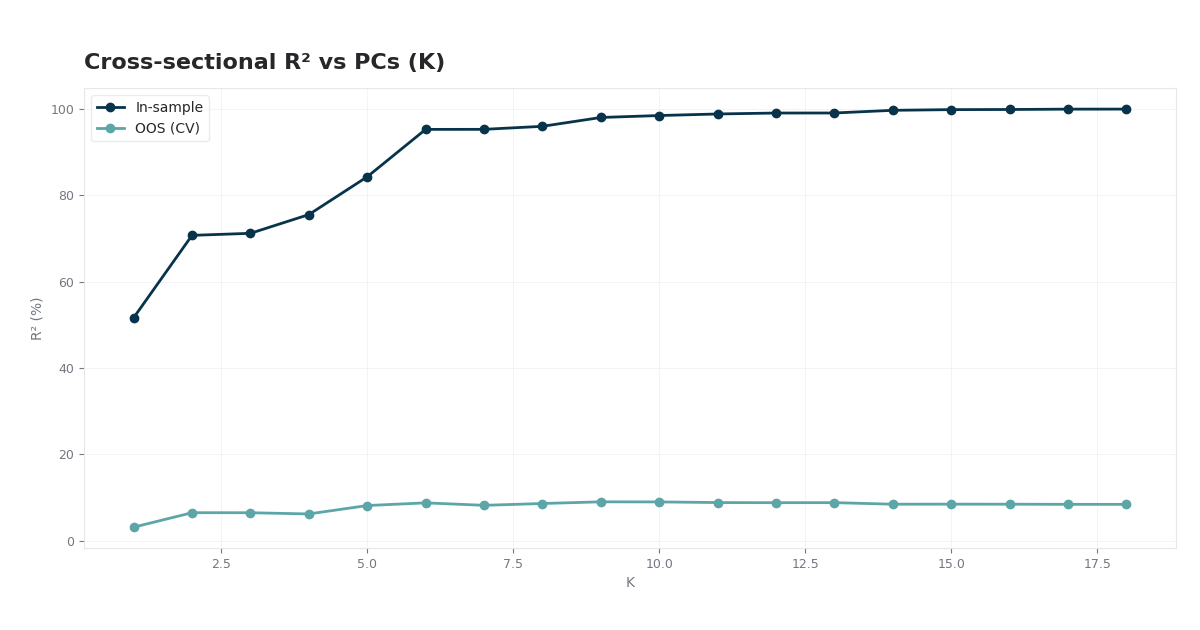

| 12. |  Cross-section shrinkage lab (ETF panel)

(2026 )

Yahoo Finance ETF panel: PCA spectrum, cross-sectional R² vs K, pseudo-OOS folds, ridge diagnostics. JSON from npm run data:shrinking-cross-section. Python, Recharts, PCA, shrinkage, cross-sectional R² |

| 13. |  Portfolio Stress Lab

(2026 )

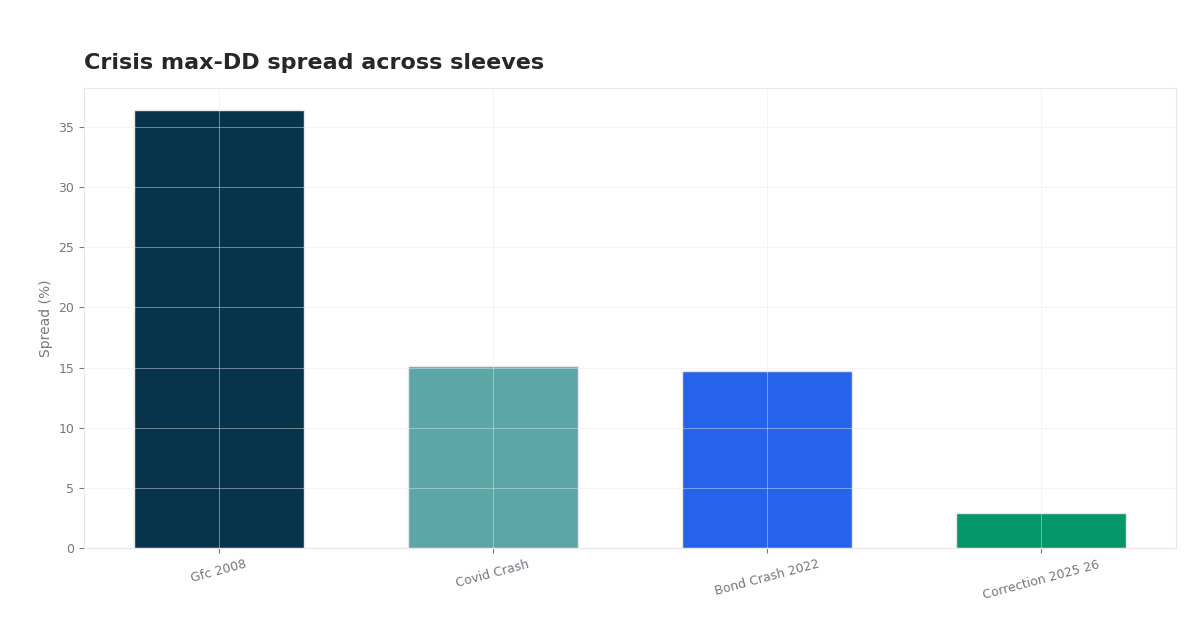

Institutional portfolio stress laboratory: historical crisis replay, univariate and compound parametric shocks, historical/parametric/Monte Carlo tail risk, Fully Flexible Probability reweighting, forward GARCH simulation, and cross-study tail-risk attribution. Crisis replay · compound stress · VaR/ES suite · FFP reweighting · regime correlation |

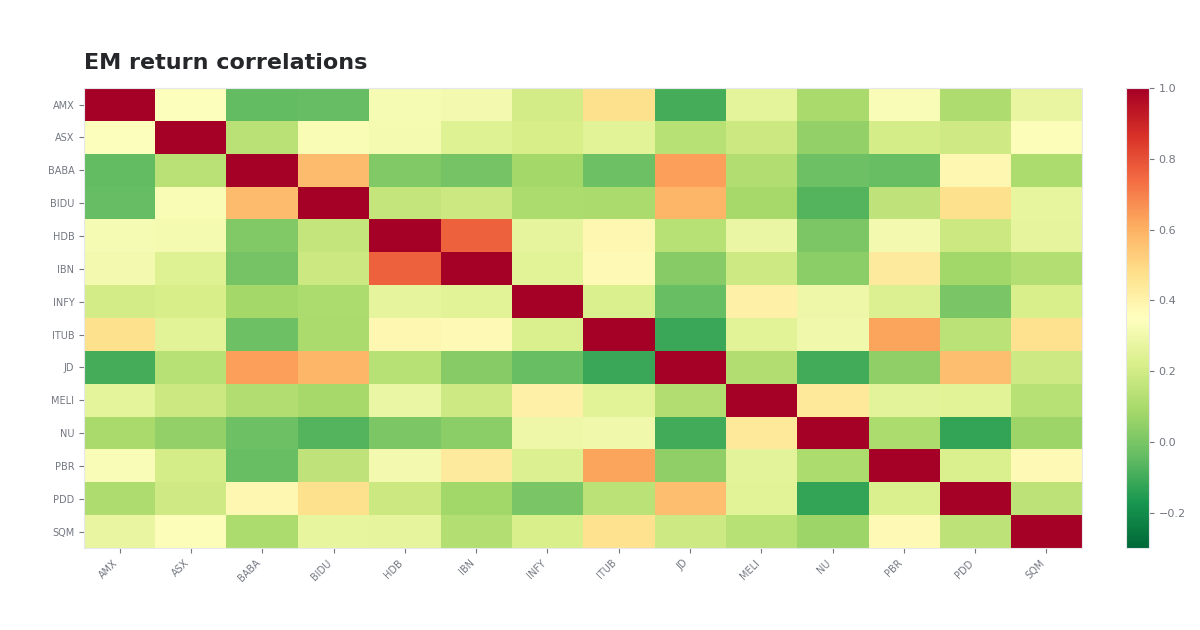

| 14. |  Emerging Markets Fundamental Portfolio

(2026 )

Multi-country EM equity framework: value/quality/risk/stability composite scoring, country–sector neutralization, constrained mean-variance optimization, correlation analytics, quintile monotonicity, and quarterly backtests vs EEM. EM fundamentals · MVO · correlation matrix · hypothesis tests · quintile analysis |

| 15. |  Market Homogeneity from Correlation Networks

(2026 )

Empirical US study of market-wide co-movement: monthly homogeneity index from correlation networks, regime analysis, SPY conditioning, and interactive network graphs. Correlation networks · homogeneity index · regime analysis · SPY overlay · network graphs |

| 16. |  Global Capital Flow Intelligence System

(2026 )

Multi-asset framework inferring global capital allocation from Yahoo Finance ETFs: eight flow engines, composite scores, regime detection, correlation networks, and flow-based portfolio backtests. Capital flow inference · 8 analytical layers · regime detection · flow portfolios · hypothesis tests |

Showing 9–16 of 40 projects